[ad_1]

scanrail/iStock via Getty Images

Investing In Tech Stocks In 2022

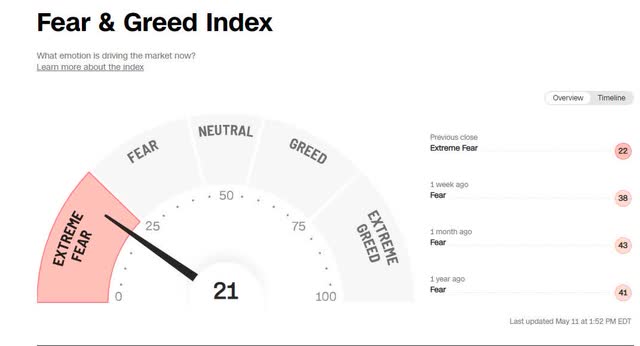

Everything is getting thrown out, including the baby with the bathwater! Fear is moving the markets, and it seems as if even those stocks with great underlying fundamentals don’t matter because all focus is on inflation, interest rates, and the Fed’s reactive stance towards monetary policy.

Fear and Greed Index (CNN Fear and Greed Index)

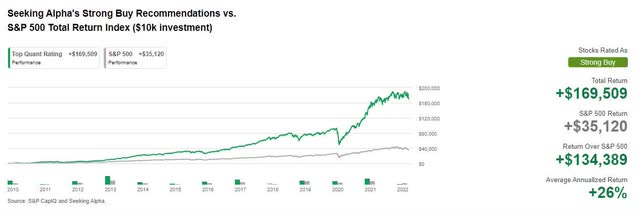

High inflation refuses to dissipate, creating further investor anxiety. Yesterday’s CPI report may mean the Fed has to get more aggressive in tightening monetary policy to curtail inflation. More aggressive rate increases or balance sheet reductions could spell bad news for tech stocks, especially those lacking profitability. We want our readers to proceed with caution. Consider a close look at stocks’ overall fundamentals, quant ratings, and factor grades. Popular and mega-tech stocks have plenty of hype, but many lack solid fundamentals. I like to focus on names that possess great metrics and pose excellent buying opportunities, especially those that have experienced some of the declines in the markets. Seeking Alpha’s Quant Strong Buy Recommendation stocks have beaten the S&P 500 Total Return Index massively over the last 12 years, generating an annualized return of 26%.

Seeking Alpha’s Strong Buy Recommendations vs S&P 500 Total Return Index (Seeking Alpha Premium)

As ranked by quant metrics and processed by a sophisticated trading algorithm, our top technology stocks are great buying opportunities and offer terrific fundamentals. Proceed with caution as you invest in this sector, but we’ve selected some excellent names in tech that have been beaten down and stand to benefit significantly when the market rotates back to investment fundamentals from fear and panic. These stocks are ready to rebound.

3 Best Tech Stocks To Buy

Fear continues to move the markets, with investors preparing for recession following the Fed’s announcement that a 50-basis point hike is necessary at the next three FOMC meetings to ‘tame inflation.’ While the market briefly experienced a raging bull after the May 4th, Fed declaration that rates would not go up 75 basis points, the short-lived 24-hour rally soon lost steam, with the indexes plummeting, erasing the Nasdaq’s 30-year bull run gain that topped 4,000%. But it is important to note that tech is not dead, and we have the name of three beaten-up tech stocks that may deliver strong returns over the long term.

Index Returns (S&P 500, DJI, and NDX) Following Fed’s 5/4/22, 50-Basis Announcement

Index Returns (S&P 500, DJI, and NDX) Following Fed’s 5/4/22, 50-Basis Announcement (Seeking Alpha Premium)

1. Alpha and Omega Semiconductor Limited (NASDAQ:AOSL)

-

Market Capitalization: $1.03B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/11): 13 out of 603

-

Quant Industry Ranking (as of 5/11): 4 out of 64

Semiconductors are some of my favorite tech stocks as many are in everyday use items from smartphones, computers, medical devices, electronics, and solar panels to electric vehicles. They are in high demand for our most precious and preferred items. In addition to daily use, chip shortages have caused semiconductors to fare well throughout the pandemic leading to a great deal of upside despite supply chain shortages. Alpha and Omega Semiconductor Limited is an international designer and developer of power semiconductor products used in high-volume applications like computers, televisions, smartphones, etc. Ranked in the top 10% (according to our quant ratings) in its sector and industry, AOSL is down 45.28% YTD, crushed like most others in the tech sector, but primed for growth and profitability, still possessing an A for momentum. This tech stock consistently outperforms its sector peers.

AOSL Momentum (Seeking Alpha Premium)

This chip has room for upside. The stock possesses excellent characteristics with upside potential for both revenue and EBITDA growth, but it also comes at a major discount. Despite the stock experiencing a decline YTD along with the rest of its sector, the markets, and Nasdaq, AOSL’s price performance over the six-month, nine-month, one year outperforms its peers. Comparing AOSL’s one-year price return to the Nasdaq and S&P 500 chart below shows there are compelling fundamentals why we rate it a strong buy.

AOSL Price Return Vs. S&P 500 & Nasdaq

AOSL Price Return vs S&P 500 vs Nasdaq (Seeking Alpha Premium)

Alpha and Omega Valuation

AOSL has an overall A+ valuation grade, with stellar underlying valuation metrics. The Forward P/E ratio of 7.98x is 55.66% lower than its sector peers, and the PEG ratio is -99.54%. AOSL showcases strong EV/Sales and EV/EBITDA figures. The stock is currently trading below $35/share.

AOSL Valuation (Seeking Alpha Premium)

In 3 FAANG-Less Tech Stocks For The Long Haul, I wrote that AOSL is rated a strong buy, given its solid growth and valuation ratings, superior profitability, and a rising earnings outlook. The stock is down YTD by more than 40%. Yet, it still possesses tremendous investment fundamentals. Let’s take a look at its growth and profitability metrics.

AOSL Growth & Profitability

Following its Q2 earnings that crushed estimates, AOSL stock jumped +12%, having beat top and bottom-line figures and the most recent Q3 2022 earnings were not different, also beating estimates. EPS of $1.34 beat by $0.16, and record revenue of $203.24M beat by $9.21M (20.11% YoY). Because the company is still facing pandemic lockdowns in China and Shanghai of their packaging and testing facilities, AOSL is anticipating lower June revenue which is expected to grow 20% year-over-year. AOSL has started to outsource some of the production and manufacturing to make up for the impacts and plans to remain on track toward their $1B annual revenue goal.

AOSL Growth Grade (Seeking Alpha Premium)

Along with analysts, management shares growing conviction. The computing segment has experienced strong demand.

“Revenue [in the computer segment] was up 28% year-over-year, up 2% sequentially, and represented 44% of our total revenue. These results were somewhat stronger than our prior expectations as the March quarter is typically our seasonally weakest quarter following strong holiday shipments. The main driver of this outperformance was continued strength in notebooks, particularly from OEM customers that have a higher concentration of their business serving commercial laptop applications.

We believe this was driven by return to office trends and company’s refreshing employee work laptops. We deliberately targeted a higher mix of commercial projects during the past years since our power ICs and power MOSFETs have higher performance specifications and higher prices that better suit commercial markets. This benefited us as the consumer market is beginning to see weakening demand.” -Steven Chang, AOSL President.

As AOSL’s executive team and financials continue to make strategic improvements to grow, it outperforms its tech peers. Given the tailwinds we see for the semiconductor industry and the explosion of data, our next stock pick should come as no surprise.

2. Micron Technology, Inc. (NASDAQ:MU)

-

Market Capitalization: $78.56B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/11): 15 out of 603

-

Quant Industry Ranking (as of 5/11): 5 out of 64

A worldwide leader in semiconductor memory solutions Micron Technology Inc. designs, manufactures, and sells the memory chips used in smartphones, personal computers, servers, and other products. Considered one of the most innovative providers of memory solutions, MU developed an industry-leading 1-alpha DRAM process technology that provides faster-operating speeds for mobile platforms and several improved memory density technologies. Despite this ingenuity, the stock trades at an amazing discount to the sector and it provides a strong valuation framework.

MU Valuation (Seeking Alpha Premium)

MU is down 30% YTD, trading more than 60% below its sector, with a forward P/E ratio of 7.15x and a PEG ratio nearly 90% below its peers. This stock pick is very attractive with an excellent balance sheet and B+ Valuation Grade.

Factor Grades Instantly Compare A Stock’s Investment Characteristics To Its Sector

MU Factor Grades (Seeking Alpha Premium)

Micron Technology is another semiconductor company benefiting from global chip shortages and is a substantial buy opportunity with an excellent valuation and reputation. MU possesses great fundamentals, evident in Seeking Alpha’s factor grades above. Because data centers are one of the biggest memory and storage markets, Micron grew its revenue 25% to $7.79B from January 1 to March 3, 2022.

“Micron is looking at a record year in fiscal 2022…Our end-market demand is strong, our customers’ demand is strong, and supply is constrained,” said Micron Chief Executive Officer Sanjay Mehrotra.

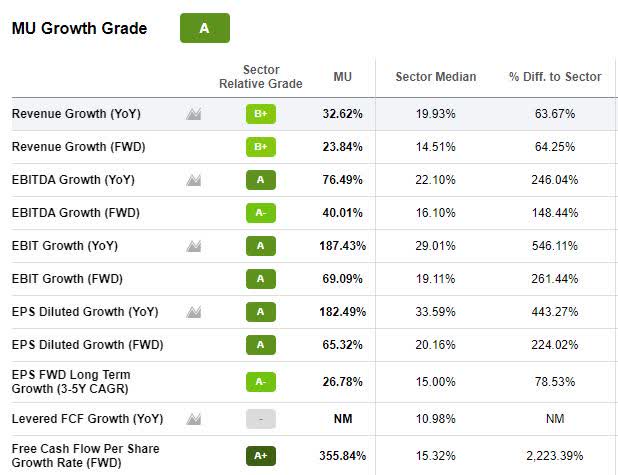

MU Growth & Profitability

MU continues to beat both top- and bottom-line earnings for the past 13 quarters. The most recent Q2 2022 Earnings resulted in an EPS of $2.14, beating by $0.16, and revenue of $7.79B, beating by $241.85M (24.86% YoY) prompting 25 FY1 Up analyst revisions. Below, the growth grades indicate that MU is one of the fastest-growing IT companies possessing 355.84% Free Cash Flow. It is also one of the most profitable in its profitability grades, with $15.01B Cash from Operations.

MU Growth (Seeking Alpha Premium)

In addition, its stock repurchasing MU declared its $0.10, payable last month. With the likes of J.P. Morgan forecasting 8% DRAM growth for the chipmaker, MU’s financial strength is being highlighted throughout the market. Wall Street Analyst J.J. Park noted,

We have revised up our 2022 memory revenue estimate by 8%, including 7%/11% upward revisions to DRAM/NAND revenue, respectively.

Because NAND (a type of flash storage technology) is anticipated to outgrow the DRAM market, Micron’s restructuring and ahead of the game mentality has successfully delivered its products in advance and at discounted prices to competitors, Samsung and SK Hynix while trading at a discount.

Although Micron faces competition from firms like Samsung and SK Hynix, it should continue to gain from global chip shortages. As a leader in the industry, MU is the most opportune of the semiconductor stock picks. But we have another chip stock worth considering.

3. Daqo New Energy Corp. (NYSE:DQ)

-

Market Capitalization: $3.13B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/11): 14 out of 603

-

Quant Industry Ranking (as of 5/11): 1 out of 31

Full disclosure, DQ is not Dairy Queen, and this recommendation will not be as welcomed as their beloved soft-serve ice cream or Blizzard treats. Daqo New Energy Corporation and its subsidiaries are leading manufacturers and sellers of low-cost, high-purity polysilicon to manufacturers of solar power products, globally. Headquartered in China, there it is, DQ is a leading clean energy company with tremendous growth and consistent production and sales volume.

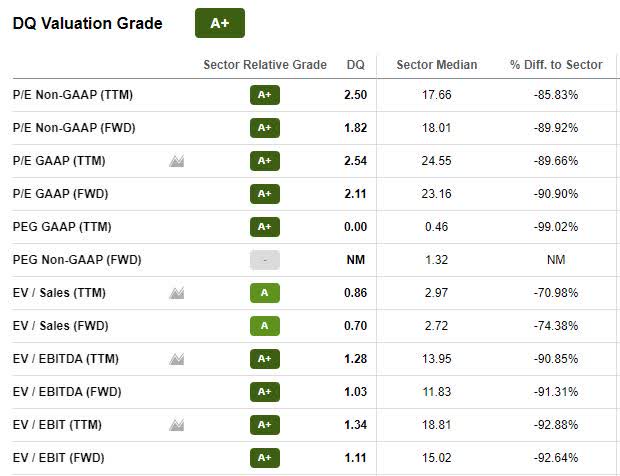

DQ Valuation

Like the other two stock picks, DQ has experienced a decline amid market fears. Being down only 10% YTD may seem like this stock is an outperformer. However, on a 52-week basis, the stock is down 50%, fully reflecting the pandemic, supply chain issues, and the China card. Trading at $37.58/share, which is near its 52-week low of $32.20, this semiconductor equipment stock is ripe for the picking, especially at the A+ valuation grade below.

DQ Valuation Grade (Seeking Alpha Premium)

This stock has excellent growth and profitability prospects. In addition to P/E ratios more than 80% below its sector peers, DQ’s current PEG ratio is 99% below than its sector peers, indicating that now may be an excellent opportunity to buy. But if that’s not enough to convince investors, J.P. Morgan prompted a 10% DQ rally after upgrading the stock from Neutral to a $55 price target.

DQ Growth & Profitability

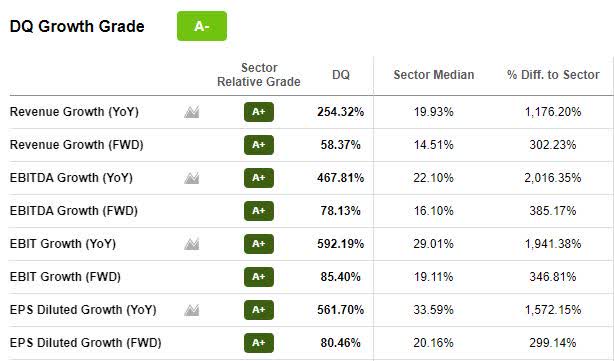

Within the last 90 days, eight analysts have revised upwards their estimates for DQ’s earnings this year. Despite recent EPS of $6.99 missing by $0.08, revenue of $1.28B beat by $98.45M (399.94% YoY). As you can see below by the stellar A+ underlying growth metrics, this is a real growth stock.

DQ Growth Grade (Seeking Alpha Premium)

During the Q1 2022 Earnings Call, Daqo CEO Longgen Zhang said,

“We recorded $1.3 billion in revenue, also more than 3x of the revenue for the fourth quarter of 2021, and we recorded operating income of $797 million, net income attributable to Daqo New Energy shareholders of $536 million, earnings per share of $7.17 per share and EBITDA of $827 million, all representing substantial sequential and year-over-year growth.

At the end of the quarter, our combined cash, short-term investments, and banknote receivable value reached $2.6 billion, an increase of $1.2 billion compared to the end of last year. This strong financial performance reflects not only the strength of the end market but also the trust that our customers place in the quality and reliability of our high-purity mono-grade polysilicon products.”

DQ Profitability Grade (Seeking Alpha Premium)

Daqo believes that the polysilicon sector is one of the most profitable in the solar chain and will continue to outproduce its peers. Gross profits are stellar, as evidenced above. Gross profit of $813.6M compared to the $239.8M of Q421 and Gross margin saw a 290-basis point increase for the same period, both of which were attributed primarily to a decrease in production costs for silicon raw materials. Although wartime and lockdowns can pose a potential risk, the overall outlook for DQ remains strong, given it is a frontrunner in its market and renewable energy is the future. From a qualitative perspective, fellow Seeking Alpha Contributor Dalton Hicks writes,

“According to Mordor Intelligence, the global solar PV market is expected to grow at a CAGR of 13.78% between FY21 and FY26. Across the globe companies and people are becoming more conscious about their carbon footprint. Daqo is a leading producer (of) polysilicon, which is the main conducting component in every solar product produced. As solar energy products grow in production, Daqo will need to manufacture more polysilicon to keep up with demand. I find the global directive towards clean energy as strong qualitative aspect of Daqo’s business.”

This stock possesses excellent fundamentals and a great outlook. Like our other picks, DQ is undervalued and beaten up by fear. Consider adding these stocks to your portfolio.

The Timing May Be Right To Start Buying Beaten Up Tech Stocks

Even in a down market, tech stocks can be great buys if you identify those with fair valuations and solid fundamentals and capitalize on their growth and momentum. Our stock picks are in the semiconductor industry, they have products that are in high demand, and are a great way to ride the semiconductor wave. Each of the stocks possesses forward EBIT growth north of 70%. These are incredible growth rates. In the current environment where each of these stocks, AOSL, MU, and DQ, are trading near 52-week lows, each offers a good balance of growth and value, and buying them at their current price decline offers your portfolio the opportunity to capitalize on potential upside.

Our quant grades and investment research tools, available to Seeking Alpha Premium subscribers, help to ensure you are furnished with the best resources to make profitable investment decisions. For example, using our Quant system which evaluates the valuation, growth, profitability, momentum and analysts’ earnings revisions of each stock, here are our Top Technology Stocks.

[ad_2]

Source link

More Stories

Don’t Use an Apple AirTag as a Pet Tracker – Use a Whistle Instead!

A growing number of Samsung owners are using the same terrible password

Amazon begins layoffs of up to 10,000 jobs, blames “uncertain” economy